by scott.gillum | Feb 22, 2018 | 2018, Opinion

I hadn’t had that type of feeling in 20 years until today.

It was back in grad school. I had a professor who taught a class on entrepreneurship. He was a highly decorated Green Beret who had founded a major manufacturing company after he left the army.

As he regaled us with the story of building his company he mentioned missing the births of his children and much of their early lives. He wore it like a badge of honor, not a lick of remorse or regrets, despite having many years to reflect back.

It was awkward. I’d never seen a presenter so misaligned with an audience, until today.

I just returned from a conference about the future of technology and its impact our lives. Founded by a parent of an autistic child who had gone on an exhausting journey hoping to learn how new technology may be able to improve the child’s life.

The theme, topics, and presentations were from technology organizations that were putting purpose ahead of profits. I heard an eloquent presenter speak on using data and new insight to break the “chain of poverty” and the “pipeline to prison.”

A VR company gave a 3D game demo on how they were using virtual reality to help improve the therapeutic outcomes for autistic children.

And then came the presentation from a global communication behemoth.

Except the presentation wasn’t a presentation. It was a self-center, chest pounding, aren’t we “great” type of speech, which would have been perfectly at home at a technology conference five years ago, but felt totally out of sync today.

We heard about their history of innovation, recent acquisitions, and the billions they were investing in the US. What we didn’t hear was how their incredible technology was going to make our lives, our children’s lives, or our communities better. They lacked purpose.

You could sense the disconnect with the audience, the awkwardness was palatable. It was an uncomfortable feeling, I hadn’t had in a very long time.

Leaving the event, I was thinking maybe it’s just me and the people I associate with who are looking for something more from organizations or…maybe this company, like my professor years before…really doesn’t get it.

by scott.gillum | Feb 8, 2018 | 2018, Business Trends

In the 90’s casual Fridays brought about the slow death of formal business attire in the office place. In the new millennium, mobile devices effectively eliminated the “9 to 5” workday and erased the line between personal and professional. Now, the “Gig Economy” is about to kill the concept of a company employee.

The freelance workforce is growing three times faster than the U.S workforce. At this rate, according to a recent survey by Upwork and the Freelancers Union, independent workers will be the majority by 2027. Yes, more people will work for themselves than for corporations, and they will be doing it because the want to…not because they have to.

The work is not what you would think of as typical “gig economy” jobs, e.g. an Uber driver. According to the FIA survey of close to 6,000 adults, this group is preparing for the future more swiftly than traditional employees. Nearly half of the freelancers surveyed told researchers that their work is being impacted by AI and robotics (only 18% of the traditional workforce). As a result, 65% are staying on top of the latest trends and are putting time aside to learn new skills, compared to 45% of traditional corporate employees.

As a result, this specialized workforce is finding independence because it is developing high demand, hard to find skill sets, creating an opportunity for them to offer their time to the highest bidder. Rather than work on projects dictated by an organization for a set salary, they can choose to work on various projects based on their interest for multiple companies. Selecting projects that advance or refine their skill sets. Deepening their experience that increases market value. This practice, commonly seen among IT workers, is now making its way into other areas like marketing and HR because of the increased use of digital tools and platforms.

It’s not only employees who are driving this trend. Employers see this as an opportunity to optimize their staff cost. The “Open Talent Economy” described by Deloitte is expected to grow significantly in the next 3-5 years. According to their research “off-balance” sheet employees will grow 66 percent over that time period. While only 6% of the C-Suite rated this trend a priority in 2017, 26% believe it will be important in the next 3-5 year, an increase of 400 percent, one of the largest increases seen in their annual Global Human Capital Trends report.

Sitting between, and enabling these trends are digital platforms like Upwork, BTG and Carbon Design which are enabling this transition. In the recent McKinsey Global Institute report, A labor market that works: Connecting talent with opportunity in the digital age, McKinsey states that these platforms could boost global GDP by $2.7 trillion by optimizing the match between work and employees, and by pulling 47 million inactive people (globally) into the workforce. As the US reaches full employment these “inactive workers” will be a critical source of labor capacity.

Unemployment fell to a 20 year low in Q4 of 2017, now standing at 4.1. A tight labor market will increase competition and opportunity for employees with specialized “in demand” skill sets. Talent now has leverage; however certain items may slow this revolution in the workplace.

Healthcare coverage is the primary one, retooling and training of inactive workers being the other. Look for these talent platforms and AI to play a role in resolving those challenges in the future. Additionally, changes to regulatory frameworks, corporate practices, and individual mindsets, may be required according to McKinsey’s research.

One thing is certain, the forces behind this transformation are accelerating driven by the recent tax changes. Apple and Amazon have announced they will be creating tens of thousands of jobs in the US. Added that amount of new positions to an already tight labor will force us to think about how work is done, and who does it. The jobs may be here but where the “work” gets done may not. We may not only see the “death” of the company “employee” but also the concept of a “domestic” workforce.

For more articles and insights like this delivered straight to your inbox, sign up here!

by scott.gillum | Dec 11, 2017 | 2017, Marketing

We are in a “Digital Revolution” as futurist Ray Kurweil stated in a recent interview. With machine learning, artificial intelligence (AI), and cognitive computing enabling everything from Apple’s new IPhone X to autonomous driving vehicles, it’s hard not to talk about the technology. And considering the herculean effort to construct and configure the tools, it’s hard to fault them for doing so.

Unlike the latest wave of technology innovators like Uber and NetFlix who disrupted industries and business models, this “Forth Industrial Revolution” brings with it a healthy dose of personal disruption. From robots to artificial intelligence, it has the potential to impact everything from how we work to how we live our daily lives. And with that comes some very real concerns about the future and our privacy.

Futurists like Stephen Hawkins and Marc Andreessen have helped give the media fuel for the fire. In an interview with the BBC, Hawkins warned that the development of “full AI could spell the end of the human race.” Andreessen has been quoted as saying that in the future there will be two types of jobs: “people who tell computers what to do and people who are told by computers what to do.”

In fact, the technologies receiving the highest amount of investment are those that are focused on making machines more “human.” According to Venture Scanner, deep learning, natural language processing and image recognition make up the top three funding categories within AI. Kurweil believes that we are only 11 years away from passing the “Turing Test,” the measure that determines if humans can detect the difference between a human or a machine.

Unfortunately, what may get lost in the noise is the great potential of this new generation of technologies. Autonomous vehicles are predicted to save 30,000 lives a year from traffic accidents. Robots are being programmed to help give the disabled more independence. Advancement in the diagnosis and treatment of certain types of cancer are already being seen and some believe that AI could lead to the end of cancer within our lifetime.

Why isn’t the focus on the benefits of these new technologies rather than on the concerns? Professor Theodore Levitt, a former professor at Harvard Business School in the 60’s may have the answer. Levitt was a thought leader in sales and marketing but may best known for the phrase “People don’t want to buy a quarter-inch drill; they want a quarter-inch hole.” The abridged version “Sell the hole, not the drill” has been uttered by sales managers for decades and it’s particularly relevant for the latest wave of new technologies.

We’re in the early stages of this “revolution” so much of the talk is about the “drill.” Explaining the process of building the “drill” is necessary for audiences like investors or partners. It’s also aimed at potential users/customers in hopes they will be able to define the holes to be drilled. The tricky part for marketers is that there are parts of the drill that have the real potential to threaten or scare audiences.

This is the tightrope technology marketers are going to have to walk for the foreseeable future. In order to develop the apps (the “holes”) marketers need to find and convert early adopters. The messaging that appeals to that audience may put others on high alert. It’s a classic “Crossing the Chasm” challenge as described by Geoffrey Moore.

Early adaptors, as described by Moore are comfortable with risk. Unfortunately, when things go wrong, like Google’s DeepMind experience with UK’s National Health Services where their initial work on mobile apps was found to have violated the UK’s patient privacy laws, it makes the “Chasm” grow between the early adopters and the early majority.

Here’s the learning for marketers, one of the four characteristics of visionaries that alienate pragmatists (Early Majority) is the overall disruptiveness of the technology. To be successful in building a bridge over the “Chasm” you may need to tone down your “disruptive” messages. Build a roadmap that gently walks them over the bridge step by step, given them reassurance along the way.

We also know from CEB/Gartner that buyers make purchase decisions based on personal value they perceive. To market “human-like” technologies to humans you have to understand their fears, concerns, and behaviors. Just because your technology can do something as well as or better than a human…doesn’t mean you need to actually “say it.”

by scott.gillum | Dec 5, 2017 | 2017, Entrepreneurship

This is the view from my standup desk. On some days, I stare out the window at Regan National and fantasize about flying off to an exotic location as a result of the wide success of the new business. On other days, I think about getting on a plane and running away from it all. That pretty sums up my first 30 days. Ping-ponging between extreme highs and lows, and never feeling like I’m going fast enough.

This is the view from my standup desk. On some days, I stare out the window at Regan National and fantasize about flying off to an exotic location as a result of the wide success of the new business. On other days, I think about getting on a plane and running away from it all. That pretty sums up my first 30 days. Ping-ponging between extreme highs and lows, and never feeling like I’m going fast enough.

In my last post, I used the analogy of running up a hill, here are some of the things I’ve learned in the early part of this journey.

- Commute – Now that I no longer paid parking I’m now a mass transit user. My commute to the office used to be an hour via the backroads. It’s now a 40 minute (on most days) Metro ride. Have to say, I don’t miss driving, in fact, getting back in the car holds no appeal at all. On the rare occasion I need to drive to work I tap my Parking Panda app and park in the garage across the street for half the listed daily rate.

- Office – For three years I was a mentor at the startup incubator 1776. Now I’m a member. Settling in I’ve been surprised by the other entrepreneurs in resident. Or in other words, I’m not the only old guy among the twenty-somethings. In fact, there may be the same amount or more of us. It’s also not all startups. Accenture Digital is here, and a major health network and venture capitalist from Israel.

- Tools – holy cow, there are so many low or no cost tools available it’s hard to cover them all. Here are a few that you might want to check out. Try MeetUp which was recently acquire by WeWork for expanding your network, learning new skills, meeting like-minded folks. If you are a retail business try Alignable for building a referral network. No longer have someone to review your proposals sign up for Grammarly. How about an assistant to manage your schedule try Calendly. If you have remote employees you have to have Slack. You’ll need a domain, a website and email. I got everything from one provider, GoDaddy but there are other sites like Verisign and Web.com.

- The team – you’ll need an account, lawyer and banker. In addition to family and friends! Some will be your guides, others your cheerleaders and on certain days, both.

- Inspiration & Insight – by coincidence, I happen to be reading two books that have been very helpful in various ways. The first, Chaos Monkeys is about the startup environment in Silicon Valley. Great insight (and entertainment) regarding various funding methods, understanding investors, dealing with team members, and the long and bumpy startup road. If you’re doing anything in the Tech space this is a must-read. The second entitled Will It Make The Boat Go Faster is a business management book (goal setting, success drivers, overcoming challenges, taking risks, motivating teams, etc.) told through an inspiring story of a British Olympic rower’s quest for a Gold Medal at the 2000 games in Sydney. If you think the startup life is hard, try being an Olympic athlete. It helps keep things in perspective — this quote from the chapter on Risk has been particularly comforting…”The most conservative, boring person living the greyest of lives is taking as many risks as the adrenalin junky free climbing on a high rock race. The difference is the type of risks they are taking.”

- The paperwork & process – if you’re thinking about venturing out on your own here are some of the forms, legal documents, and agreements you’ll need. If I only knew what I know now…

- Memorandum of Understanding (MOU) – in my case I have an international investor so the first step for us was to get to the MOU which laid out the terms of our agreement including, ownership, investment commitment and the business model.

- Certification of Formation – the next step was then registering the business. We registered the business as a Limited Liability Company (LLC). As part of this process, you will also need an LLC Operating Agreement form and Organization Meeting if registering as a Sole Member of the LLC.

- Tax ID – now that the business is registered go to the IRS.gov site and get an EIN (Employer Identification Number) which is essential for setting up your bank account and tax purposes.

- Business Bank Account Forms – if you’re registering as an LLC you will need 1) the Certification of Formation, the Operating Agreement and the IRS letter with your EIN

- Register the Business in the State of Operation – my business is registered in Delaware but operates out of Virginia which required filling out an application for a Certification of Registration to Transact in Virginia. You will then receive an ID and DCN (Declaration Control Number) for tax purposes and a DCN number. Also, check with your county and/or city for additional registrations and tax liabilities.

- Operating Agreement – this document turns the MOU into a legal agreement. It contains more detail relating to the management and operation of the company, (liabilities, tax obligations, ownership structure, dissolution, etc.) It’s also critical for unlocking investment in the organization.

- Other Documents – you’ll need a W-9 and business insurance. Check with your homeowner or car insurance provider you may find they offer business insurance as well…mine did.

I’ll be back in 120 days to give you another update on #buildingcarbondesign.

by scott.gillum | Oct 31, 2017 | 2017, Marketing

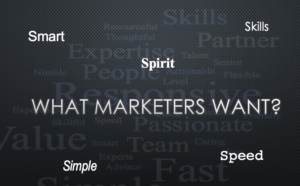

We’ve tried surveys, but they say one thing and then do another. One on one sessions, yep, tried those as well. How do we really know what our clients want? Over the last few months, I’ve had the opportunity to speak with close to fifty marketers, friends, clients and former colleagues. I didn’t have an agenda or a pitch, just a conversation about their career path and how they decided on their professions.

We’ve tried surveys, but they say one thing and then do another. One on one sessions, yep, tried those as well. How do we really know what our clients want? Over the last few months, I’ve had the opportunity to speak with close to fifty marketers, friends, clients and former colleagues. I didn’t have an agenda or a pitch, just a conversation about their career path and how they decided on their professions.

The conversation eventually made its way into a discussion of relationships they had with various consultants, advisors, and agencies. Just for kicks, I built a word cloud from my notes and saw five themes emerged around what they wanted from a vendor — I call it the five “S’s”.

- Smarts – this was a common theme — “I don’t want to have to explain my business to the vendors that I work with. They need to do their homework.” Almost every conversation had an element of the client wanting vendors to be up to speed when the engagement started. Time is money and clients don’t have the time (especially on their dime) to get you up to speed. And, for big consulting firms and agencies, don’t get comfortable with thinking you have a lock on all the brightest folks. They use plenty of very smart individual contractors. Many of them, just came from your world.

- Skills – similar to the above comment, clients want to work with agencies and consultants that have the skill sets that they can’t find, hire or retain. This was especially important when it came to digital talent. They have made investments in MarTech but are having a hard time finding the talent to optimize, or even operate, the technology…and it is becoming more difficult.

- Speed – “I need the vendors I hire to operate at the speed of my business,” said the CMO of a Fortune 50 hi-tech firm and others echoed her comment. There were also comments related to responsiveness. If you’re standard policy is to respond to a clients’ email within 48 hours, you’re about 40 hours off on their expectations. Being more responsive can buy you time on deliverables. Clients want to know, or at least feel, like you’re making progress on their effort. Gaps in communication create the risk of your client feeling like they are not getting the attention they deserve or pay for…and they know when you’re stretched too thin.

- Simple – combine Smarts with Speed and you get Simple or at least that is what the client would love. They want to be able to understand your recommendations so they know exactly what decisions, or action, to immediately execute. Consultants — they are tired of the upsell, where one problem suddenly surfaces another problem, especially when they haven’t received the output of the first project. Agencies — the more complexity you add to a campaign the longer clients believe it will take to execute. Smart, valued vendors take complex problems and make them simple to understand and resolve. They know they have other issues they just need to address the problem in front of them.

- Spirit – this one surprised me and took some time to understand. The core of this theme was rooted in marketers stating that they wanted to work with vendors who were “enthusiastic” about their business, or “passionate” about their own jobs/role. They want a partner who brings some fun and/or passion that may be lacking in their organization. If you are pitching an idea an important part of the “sell” job is how you deliver it. If you’re not excited about it, they won’t be either. The last thing you want is a client who doesn’t want to talk to you because they know it won’t be enjoyable…they have plenty of those meetings internally. Be their break in the day, the good news, the breath of fresh air they so desperately need…especially at the end of the day or week.

Surprisingly, I didn’t hear cheaper. Don’t misunderstand, they want value and recognize that to get it they have to make the investment. Now that you know what they really want that shouldn’t be a problem to deliver, be the bright spot in their day.